Why AI Is Finally Making Payment Audits Scalable

Executive team gets asked the same question: why are payment costs rising when volumes look stable. The uncomfortable answer is that payment economics rarely change in one big, visible step. They drift through complexity. New channels launch, routing is left on default, tokenisation changes the mix, fee tables update, disputes rise, and reporting stays fragmented. AI is now making payment audits scalable by turning this complexity into an ongoing, measurable control, giving global CxOs a practical way to protect margin without turning payments into a permanent fire drill.

Payments oversight is shifting from periodic audit to continuous control

Payments teams have always lived with a quiet contradiction. Payments sit at the centre of almost every customer experience, yet many organisations still run payment oversight like a periodic compliance exercise. Meanwhile, payment cost, risk, and performance can change materially week to week, driven by routing decisions, network and scheme pricing updates, acquiring markups, tokenisation behaviour, and product shifts such as wallets, subscriptions, and new pay later models.

For global CxOs, this matters because payments are no longer a back office utility. They are a margin line, a customer experience lever, and a risk surface. A single transaction may touch the point of sale or checkout, a gateway, an orchestrator, a fraud tool, an acquirer, a network, an issuer, and multiple data enrichment layers. Each layer can add cost and complexity, and each can hide issues that only show up when someone has the time and specialist capability to reconcile and validate the detail.

This is the moment where artificial intelligence is moving from headline promise to practical leverage. AI is not replacing payment expertise. It is making payment audits scalable by doing what humans struggle to do at scale: ingest messy data, reconcile mismatched records, detect anomalies early, and translate complexity into a narrative that supports executive decisions. It shifts payment governance from a post-mortem to an operational discipline.

Payment audit meaning: what you are really trying to answer

Most organisations say they want a payment audit, but what they actually need is executive clarity on a small set of questions that drive profit and risk.

What are we paying, to whom, and why. Which costs are variable, which are negotiated, and which are embedded in the model. Are we routing payments in a way that matches commercial goals, or have we drifted into a default configuration that made sense in a different business context. Are we carrying silent leakage through misclassification, outdated fee tables, duplicate charges, or hidden markups. And can we explain our payment economics in a way that allows the CEO, CFO, and COO to act with confidence rather than relying on assumptions.

A good audit is not a spreadsheet exercise. It is a story backed by evidence. It connects contract terms to real outcomes, and it identifies the levers that actually move the number. In the Payment Matters world, the objective is to uncover hidden fees, simplify complexity, and build smarter payment strategies that translate into measurable cost and performance improvements.

Why traditional payment audits do not scale

Payment audits are hard because payment data is fragmented and the rules change frequently. Settlement files, acquirer statements, gateway logs, point of sale exports, and fraud decisioning events often do not share consistent identifiers. Time zones differ. Refunds and chargebacks arrive on different cycles. Partial approvals and split fulfilment create edge cases. Tokenisation can cause a single customer instrument to appear under multiple identifiers over time.

Even when the data can be assembled, the effort is usually manual. People perform lookups, pivot tables, and ad hoc reconciliations. That work tends to be done by a small number of specialists who understand the quirks of each provider. The result is that audits are infrequent, late, and too narrow. They focus on a sample, a short time window, or one provider. Leakage persists because the organisation does not see problems early enough to fix them, and it cannot keep monitoring once the audit ends.

This is also why payment audits often become a negotiation tactic rather than an operational capability. The audit produces a list of issues, but the business cannot continuously validate the impact of changes that follow. Over time, pricing drifts again. New products launch. New channels appear. The audit becomes a cycle rather than a control.

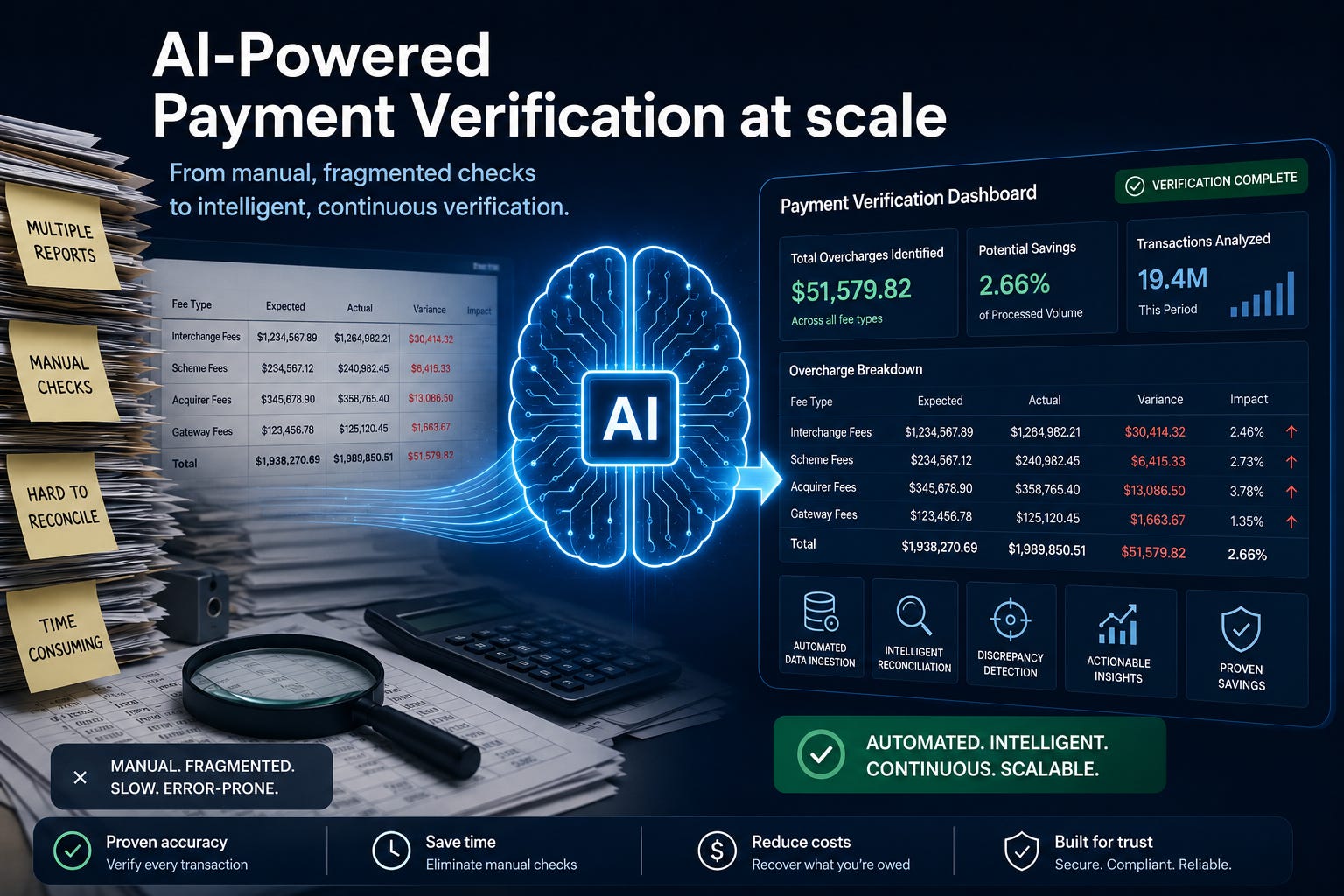

How AI makes payment audits scalable: from detective work to continuous control

AI makes payment audits scalable by turning the audit into a repeatable system. In practical terms, that system has four capabilities that matter for payment governance, cost of acceptance, and executive confidence.

First, it normalises data. AI assisted extraction and classification can map different file formats and naming conventions into a unified model. It can handle missing fields, inconsistent identifiers, and variations in provider statement structures. This reduces the human effort of preparing data and enables more frequent review without increasing headcount.

Second, it reconciles transactions. Payment teams often spend most of their time answering basic questions such as whether the order and settlement match, whether the refund was processed correctly, and whether fees were applied as expected. AI can learn reconciliation patterns, handle fuzzy matching across timestamps and references, and flag exceptions that truly need attention. That is the bridge from periodic review to ongoing assurance.

Third, it detects anomalies. The value of an audit is not only in understanding average cost. It is in catching the outliers that drive leakage and risk. AI can identify sudden shifts in effective fee rates, unusual chargeback patterns, unexpected declines, or routing behaviours that do not align to policy. A human can spot an issue in a sample. AI can monitor the whole population and identify issues early enough to prevent weeks of margin leakage.

Fourth, it translates findings into actions. Payment data is often technically correct but commercially unreadable. AI can summarise findings in plain language, propose root cause hypotheses, and draft the operational tasks that follow, such as fee table validation, contract term review, routing policy updates, or provider escalation. The result is faster action, tighter accountability, and fewer unresolved exceptions.

Combined, these capabilities change the economics. The audit is no longer a bespoke project. It becomes a continuous control loop.

Payment processing fees: AI makes cost of acceptance measurable again

Most payment cost discussions deteriorate into averages, because averages are easy to compute and hard to challenge. But cost of acceptance is not an average. It is a distribution. It varies by card type, merchant category, authentication method, tokenisation, channel, geography, and acquirer setup. It also varies by the commercial construct. Some merchants pay blended rates. Others pay interchange plus plus. Some have scheme or network fee pass-through. Some have markups embedded in service fees.

Payment Matters has repeatedly focused on the need to break down components of processing fees, understand markups, and surface hidden costs in agreements, because that is where negotiating power starts. AI operationalises that philosophy by automating the classification of fees and continuously comparing billed charges to expected charges.

For CxOs, the point is simple: if the business cannot explain why cost is changing, it cannot manage cost. AI supported audit capability makes it possible to attribute cost correctly, separate mix effects from provider effects, and create a credible baseline for commercial negotiation.

Payment cost reduction: where AI creates immediate ROI for the C-suite

If there is one area where AI can deliver quick value, it is payment fees and cost reduction. Most organisations already have the data, but they do not have the capacity to convert it into accurate, timely insight.

AI supported audits can identify fee misclassification, missing negotiated exemptions, and pricing applied to the wrong segments. They can detect routing drift, where transactions are no longer flowing through the intended lower cost paths. They can highlight provider statement errors or duplicate charges. They can quantify the cost impact of declines and retries, which often create both customer friction and incremental fees. They can isolate the segments where effective rates are highest and test whether changes in authentication, token strategy, or routing policy could reduce cost without harming approval rates.

This is also where orchestration and optimisation strategies come into play. Payment Matters has focused on how orchestration can streamline card processing and improve outcomes by making routing and provider management more dynamic.[8] AI makes orchestration smarter by supplying better signals and by monitoring the results, so optimisation is measured rather than assumed.

For procurement teams, the practical impact is equally important. AI supported audits provide evidence. They make it easier to challenge fee constructs, validate pass-throughs, and distinguish between market driven costs and provider specific costs. That evidence turns a negotiation from opinion into fact.

Conclusion: the era of periodic payment audits is ending

AI is making payment audits scalable because it changes the unit economics of oversight. It turns reconciliation and fee validation from an artisanal craft into a repeatable capability. For global CxOs, that shift is increasingly non-negotiable. Payments complexity will keep rising, and margin pressure will not ease. The organisations that win will be the ones that can explain their payment economics with the same clarity and cadence as they explain revenue, labour, and supply chain costs.

The real insight is that the winners will not be the organisations that use AI to produce more reports. They will be the ones that use AI to build a living understanding of their payment system, where cost, risk, and performance are measured continuously, issues are detected early, and accountability is unambiguous. In that world, payment strategy stops being reactive. It becomes a quiet, compounding advantage.

Enjoyed this article?

We regularly publish insights on payment strategy, risk, and governance.

🔦 Subscribe for latest insights: Payment Matters

🔍 More detailed articles and email updates: Payment Matters Articles